ORDER OF MAY 31, 2021 FROM THE COUNCIL OF BUSINESS, EMPLOYMENT, UNIVERSITIES AND SPOKESPERSON APPROVING THE REGULATORY BASES OF THE COVID LINE OF DIRECT AID TO SELF-EMPLOYEES AND COMPANIES OF THE REGION OF MURCIA, PROVIDED FOR IN THE ROYAL DECREE-LEY 5/2021, OF MARCH 12, OF EXTRAORDINARY MEASURES TO SUPPORT BUSINESS SOLVENCY IN RESPONSE TO THE COVID-19 PANDEMIC, AMENDED BY ROYAL DECREE-LAW 6/2021, OF APRIL 20

Article 1.- Purpose.

1. In accordance with the provisions of Royal Decree-Law 5/2021, modified by Royal Decree-Law 6/2021, the purpose of this Order is to apply in the Region of Murcia the subsidies of the Covid line, financed by the Government of Spain, to support the solvency and debt reduction of the private sector.

2. The subsidies provided for in this Order are final in nature and must be used exclusively to satisfy the debt and payments provided for in article 4.

Article 2.- Nature and legal regime.

1. The subsidies provided for in this Order shall be governed, in addition to the provisions of the same, by the rules established in Royal Decree-Law 5/2021, of March 12, on extraordinary measures to support business solvency.

Article 3.- Beneficiaries, requirements and obligations.

1.- The following may be beneficiaries of the subsidies provided for in this Order:

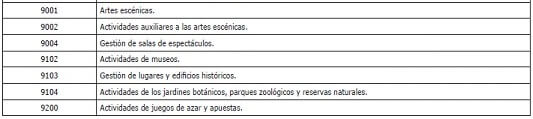

a) Entrepreneurs or professionals and entities attached to the CNAE sectors defined in Annex I, not included in letters b) and c) below of this section, and created before 2020, whose annual volume of operations declared or verified by the Administration, in the Value Added Tax or equivalent indirect tax in 2020 has fallen more than 30% compared to 2019.

b) Entrepreneurs or professionals who apply the objective estimation regime in Personal Income Tax assigned to the CNAE sectors defined in Annex I of this Order.

c) Consolidated groups that pay income tax in the consolidated tax regime whose annual volume of operations in 2020 has fallen by more than 30% compared to 2019.

Entities under the regime of attribution of income in the Personal Income Tax may request the aid when they meet the conditions for it. The direct beneficiary of the subsidy will be the applicant entity and not its partners, community members, heirs or participants.

2. Financial companies and those businessmen or professionals, entities and consolidated groups that meet the requirements established in section 1 above and that in the declaration of the Personal Income Tax corresponding to 2019 have declared a negative net result for the economic activities in which the direct estimation method would have been applied for its determination or, where appropriate, the tax base of the Corporation Tax or the Non-Resident Income Tax has been negative in said year, before the application of the capitalization reserve and compensation of negative tax bases.

3. The beneficiaries must meet the following requirements at the time of filing the application:

a) Tax domicile in the Autonomous Community of the Murcia region, except in the cases provided for in article 6.2 of the Order.

b) Accredit the exercise of an activity classified in Annex I of the Order, in the years 2019 and 2020 and that it continues at the time of presentation of the request.

c) Meet the following requirements:

-Not having been convicted by a final sentence to the penalty of losing the possibility of obtaining subsidies or public aid or for crimes of prevarication, bribery, embezzlement of public funds, influence peddling, fraud and illegal exactions or urban crimes.

- Not having given rise, for the reason for which she was found guilty, to the firm resolution of any contract entered into with the Administration.

-To be up to date with the payment of obligations for the reimbursement of subsidies or public aid.

-To be up-to-date in compliance with tax obligations and against Social Security.

-Not having requested the declaration of voluntary insolvency, not having been declared insolvent in any procedure, not being declared insolvent.

-Not having tax residence in a country or territory classified by regulation as a tax haven

4. The beneficiary at the time of submitting their request must expressly assume the following commitments and obligations:

a) Maintain the activity corresponding to the aid until June 30, 2022.

b) Do not distribute dividends during 2021 and 2022.

c) Not approving increases in the remuneration of senior management for a period of two years from the date of the resolution of the granting of the subsidy.

d) In accordance with the provisions of article 14 of Law 7/2005, of November 18, on Subsidies from the Autonomous Community of the Region of Murcia, to adopt adequate publicity of the public nature of the subsidy, through , where appropriate, from the website of the beneficiary, which will expressly include the following legend: "this company has received a grant from the Autonomous Community of the Region of Murcia through funding from the Government of Spain, to support business solvency in response to the Covid-19 pandemic ". The beneficiaries within a month from the notification of the grant award resolution must carry out the publicity described and maintain it for a period of 2 years, noting that in case of non-compliance they will proceed to request a refund of the 5% of the grant awarded.

Article 4.- Eligible expenses.

1. Expenses destined to the satisfaction of the debt and payments to suppliers, including the payrolls of workers, and other creditors, financial and non-financial, as well as the fixed costs incurred, as long as these have been accrued, will be eligible. between March 1, 2020 and May 31, 2021 and come from contracts prior to March 13, 2021.

2. The priority of payments will be as follows: first, payments to suppliers will be satisfied, in order of seniority and, if applicable, the nominal amount of the bank debt with public guarantee will be reduced, followed by the reduction of the nominal amount of the rest of the bank debt, and finally, and where appropriate, the fixed costs incurred, during the eligible period between 1 December March 2020 and May 31, 2021.

The order of seniority will be determined by the date of issuance of the invoices and / or payroll.

Article 5.- Amount of the aid.

1. Grants may not exceed the amount of eligible expenses paid by each beneficiary, within the following maximum limits:

a) In the case of businessmen or professionals who apply the objective estimation regime in Personal Income Tax, the maximum subsidy will be 3,000 euros per beneficiary.

b) For those entrepreneurs and professionals whose annual volume of operations declared or verified by the Administration, in the Value Added Tax or equivalent indirect tax, has fallen more than 30% in 2020 compared to 2019, the maximum subsidy that will be granted will be:

bi. 40% of the fall in the volume of operations in 2020 compared to 2019 that exceeds said 30%, in the case of businessmen or professionals who apply the direct estimation regime in the Personal Income Tax, as well such as entities and permanent establishments that have a maximum of 10 employees.

b.ii. 20% of the amount of the fall in the volume of operations in 2020 compared to 2019 that exceeds said 30%, in the case of entities and businessmen or professionals and permanent establishments that have more than 10 employees.

The number of employees referred to in sections b) i and b) ii above, will be calculated taking into account the average number in 2020 of recipients of monetary income from work recorded in the monthly or quarterly returns, withholdings and payments on account (model 111).

Without prejudice to the provisions of sections b) i and b) ii above, the subsidy per beneficiary may not be less than 4,000 euros or more than 200,000 euros.

It is not possible to apply to a beneficiary simultaneously letters a) and b) of this section and the provisions of letter a) prevail. Therefore, the application of the objective estimation regime in the Personal Income Tax in 2019 or 2020 implies that the beneficiary of the aid will be applied the provisions of letter a) in any case, regardless of whether carry out other activities to which the direct estimation regime applies.

Entrepreneurs or professionals who have been registered for a period of less than a year in fiscal year 2019 or in fiscal year 2020, the amount of the aid will be the corresponding amount, in accordance with the provisions of this section, applying proportionality criteria to these beneficiaries. to determine the decrease in your trading volume.

Article 6.- Compatibility of the subsidies.

1. The subsidies provided for in this Order are compatible with any other aid that the employer or professional receives or may receive, as long as the total amount of the aid do not exceed 100% of the amount of eligible expenses for the same period.

2. Groups and entrepreneurs, professionals or entities whose volume of operations in 2020 has exceeded 10 million euros that carry out their economic activity in more than one autonomous region or in more than one Autonomous City, may participate in the calls that are made in all the territories in which they operate.

3. In the case of businessmen, professionals or entities with tax domicile in the Autonomous Community of the Region of Murcia whose volume of operations in 2020 has been less than or equal to 10 million euros and do not apply the group regime in Corporation Tax only They may attend the calls made under this Order.

Article 7.- Applications.

1. The deadline for the submission of applications will be that provided for in the call established in accordance with the provisions of article 12.

2. Applications must be completed electronically through the website indicated in the call.

To submit applications, it is necessary to have one of the recognized or qualified Electronic Certificates of electronic signature that are operational in the Autonomous Community of the Region of Murcia and issued by providers included in the "Trust list of certification service providers" .

The notifications that the Institute of Development of the Region of Murcia has to make, referring to this procedure, will be made, in any case, by electronic means at the authorized electronic address (DEH) of the interested party or, where appropriate, of their representative .

4. The presentation of the application for the subsidy entails the authorization for the Development Institute of the Region of Murcia to obtain from the State Agency of the Tax Administration, the Tax Agency of the Region of Murcia and the General Treasury of the Social Security, the information provided in this Order.

6. The deadline for rectifying defects and / or presentation of the required documentation will be ten (10) business days, indicating that once the same has elapsed without correcting the lack or providing the requested documents, the request for help will be understood to have been abandoned prior express resolution of the Presidency.

Article 8.- Granting procedure.

The subsidies will be awarded under the competitive competition regime, provided for in Chapter I, Title I of Law 7/2005, of November 18, on Subsidies from the Autonomous Community of the Region of Murcia, by means of a comparison of the applications presented in which the priority criteria defined in article 9.3 will be applied, respecting the budgetary limits of the call.

Article 9.- Instruction and resolution.

1. The Development Institute of the Region of Murcia through the Processing Department will be competent for the instruction of the procedures derived from this Order.

2. The Processing Department will carry out a pre-evaluation in which compliance with the conditions imposed to acquire the status of beneficiary will be verified. Those requests that do not meet the minimum conditions imposed to acquire the status of beneficiary will be rejected in the reasoned resolution of the Presidency of the Institute of Development of the Region of Murcia finalizing the procedure for granting and rejecting subsidies.

3. The Processing Department will be in charge of evaluating and reporting the requests that have passed the pre-evaluation carried out in accordance with the previous section, establishing the priority of the requests, ordering them as follows:

a) In the first place, the applicants provided for in article 3.1.b), belonging to the sectors defined in Annex I, will be ordered in increasing order of the amount of the subsidy.

b) Once the order of priority of the beneficiaries of article 3.1.b) has been established, it will continue with the rest of the applicants according to the highest percentage of fall in the volume of operations in 2020 compared to 2019 of applicants whose activities are among the sectors defined in Annex I. In the event that more than one application has the same percentage of drop, they will be ordered taking into account and giving priority in favor of applicants who have a minor trading volume in 2020.

6. Once the final resolution proposal is approved, the Presidency of the Murcia Region Development Institute will issue a reasoned resolution for the granting of subsidies, indicating their amount, and for the rejection of applications, indicating the reason for the same.

7. When the total sum of the subsidies to be granted exceeds the available credit of the call, it may be prorated among the applications that may be beneficiaries of the subsidy under this Order, without said apportionment affecting the businessmen or professionals who apply the objective estimation regime in the Personal Income Tax, while the rest of the beneficiaries will be granted a subsidy of 4,000 euros in the order of priority until exhausting the call credit. In the event that, after compliance with this budget distribution criterion, there is a remainder of the credit without applying, said surplus will be prorated among all the beneficiaries not subject to the objective estimation regime in the Personal Income Tax.

10. The maximum term to resolve and notify the resolution of the procedure is December 31, 2021. The expiration of the maximum term without having notified the resolution, legitimizes the interested parties to understand that the request for granting the subsidy has been rejected by administrative silence.

Article 10.- Payment and justification of the subsidy.

1. After the resolution of the granting of the subsidy, it will be paid to the beneficiary, in the account number, including the IBAN, indicated in the application, by means of a single payment, in advance, exonerating the beneficiary of the obligation to provide an endorsement or guarantee, in accordance with the provisions of article 16 of Law 7/2005, of November 18, on subsidies from the Autonomous Community of the Region of Murcia.

2. The beneficiary must apply the amount of the subsidy to pay and pay the eligible expenses, provided for in the application or other eligible expenses in accordance with the provisions of article 4 of this Order, within a maximum period of two months from receipt of the amount of the grant.

3. Under the terms provided in the Resolution of the President of the Murcia Region Development Institute of January 30, 2007, published in the BORM, No. 36 of February 13, 2007, the justification of the subsidies will be made obligatorily in electronic format through the electronic address: https://sede.institutofomentomurcia.es, within 3 months from the completion of the term provided in section 2 above, using the standardized forms, which will be provided and will be available through the electronic address: https://sede.institutofomentomurcia.es

4. For grants of less than 60,000 euros, the beneficiary must justify the application of the funds received to the intended purpose by providing a simplified supporting account, in accordance with the provisions of article 75 of the Regulation of Law 38 / 2003, of November 17, approved by Royal Decree 887/2006, of July 21. The simplified supporting account will include:

- A justifying report of compliance with the conditions set forth in article 3 of this Order.

- A classified list of the expenses of the activity paid with the subsidy, with identification of the creditor and the invoice or payroll, its amount, date of issue and date of payment, or, where appropriate, loan or bank debt contract , indicating the amortization carried out, and, where appropriate, fixed costs not covered, during the eligible period between March 1, 2020 and May 31, 2021. When invoices, payroll and payment obligations are after the 13th of March 2021, the date of the contract originating the expenses must also be indicated and, if there is no written contract, request or acceptance of the offer or the budget, the date of assumption of the debt or obligation being recorded in any case. of payment.

- Details of other income, subsidies and other aids that have financed the subsidized activity, indicating the amount and its origin.

- Where appropriate, statement responsible for the publicity measure adopted by the beneficiary on its website, in accordance with the provisions of article 3.4.d) of this Order.

It is not necessary to provide a copy of the invoices, payroll or supporting documents along with the justification. However, the beneficiary is obliged to keep said documentation and provide it if required to do so in the grant verification phase or in any subsequent financial control.

The granting body, through the Processing department of the Murcia Region Development Institute, will verify, through sampling techniques on a percentage of the grants awarded for an amount less than 60,000 euros, the proof of expenditure and payment that allow Obtain reasonable evidence on the proper application of the grant. This contribution of documentation will be obligatorily made using electronic means through the electronic address: https://sede.institutofomentomurcia.es.

The Institute of Development of the Region of Murcia will verify that the beneficiary has not distributed dividends during 2021 or 2022, as well as the maintenance of economic activity until June 30, 2022.

5. For grants of an amount greater than 60,000 euros, the beneficiary must justify the application of the funds received to the intended purpose by providing a supporting account, one of those provided for in section 3 of this article, through the electronic address: https://sede.institutofomentomurcia.es, providing the following documentation together with it and by the same electronic means:

a) Invoices issued by suppliers and other creditors, as well as payrolls of workers, paid by the beneficiary against the subsidy granted. When invoices and payment obligations are after March 13, 2021, the date of the contract must also be indicated. In the case, the fixed costs not covered during the eligible period between March 1, 2020 and May 31, 2021.

b) Bank receipts of payment of invoices and / or payroll. When the creditors are financial entities, a certificate from the financial entity certifying the total or partial cancellation of the debt. It must be provided in relation to the bank debt, justification if the same has a public guarantee.

c) When the invoices and payment obligations are after March 13, 2021, contract or contracts from which the payment obligations to suppliers and other creditors derive and, in the event that there is no written contract, order or acceptance of the offer or the budget, keeping a record in any case of the date of assumption of the debt or payment obligation.

d) Where appropriate, justification of the publicity measure adopted by the beneficiary on its website, in accordance with the provisions of article 3.4.d) of the Order.

As an alternative to the presentation of the documents indicated in letters a), b) and c), their accreditation is accepted through an auditor's report as established in Order EHA / 1434/2007, May 17, which approves the standard of action for account auditors in carrying out the work of reviewing accounts justifying subsidies.

- List of the destination of the aid as established in article 4 of this Order.

- The subsidy received has been used to pay related expenses, with identification of the creditor and the invoice or payroll, its amount, date of issue and date of payment, or, where appropriate, a loan or bank debt contract, indicating the amortization made.

6. The beneficiaries of the subsidy will have the obligation to keep all the documentation required for the justification in sections 4 and 5 above, within a period of 10 years from the presentation of the justification of the subsidy in the terms provided in the same sections 4 and 5.

7. When the Processing Department of the Development Institute of the Region of Murcia competent to verify the justification of the subsidy appreciates the existence of rectifiable defects in the justification presented by the beneficiary, it will inform them, granting them a period of ten (10 ) days for correction.

8. The accreditation of any payment in cash or cash for invoices, payroll or other supporting documents of eligible expenses.

Article 13.- Advertising.

1. In application of Law 38/2003, of November 17, General Subsidies, the call, as well as relapsed concession resolutions, will be published in the National Subsidies Database (BDNS, www.pap.minhap.gob.es/bdnstrans/), as well as its extract in the Official Gazette of the Region of Murcia.

Final provision.- Entry into force.

This Regulatory Basis Order will enter into force the day after its complete publication in the Official Gazette of the Region of Murcia. Murcia, May 31, 2021.